Golden Investment Ideas

Every year, investors ask the same question in slightly different outfits: Can I beat the market without becoming a full-time lunatic? The Golden Investment Club Annual Report 2025 offers an answer that is both sobering and strangely liberating: probably not consistently … and that is exactly where clear thinking begins.

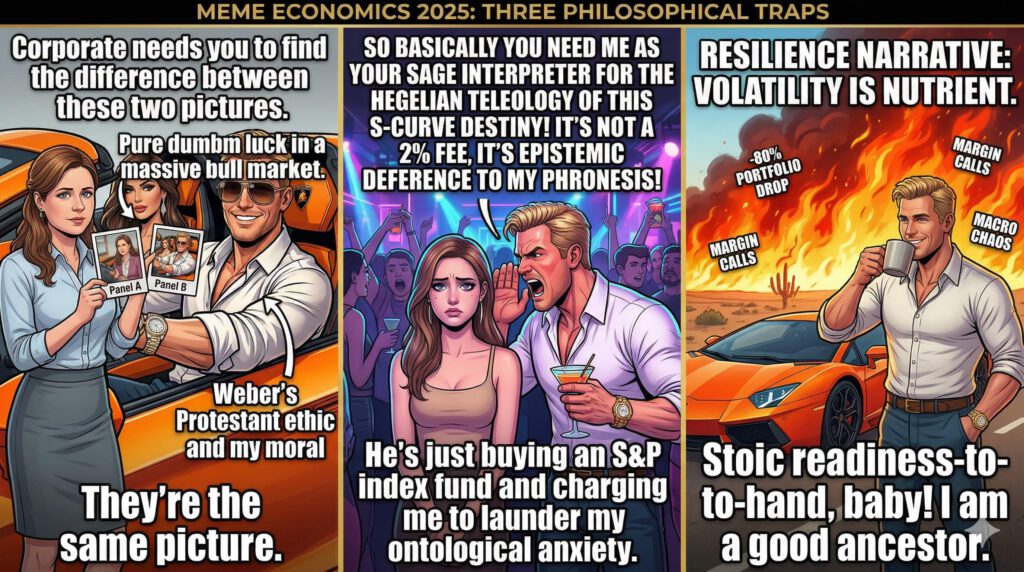

The report starts with the brutal arithmetic. Before costs, active managers as a group can only equal the market; after costs, they must lag it. This is not ideology. It is subtraction wearing a tie. The paper leans on Sharpe and Bogle to make the point that fees, turnover, taxes, and hidden frictions are not background noise — they are destiny with a decimal point. Over long horizons, “slightly more expensive” often means “materially poorer.”

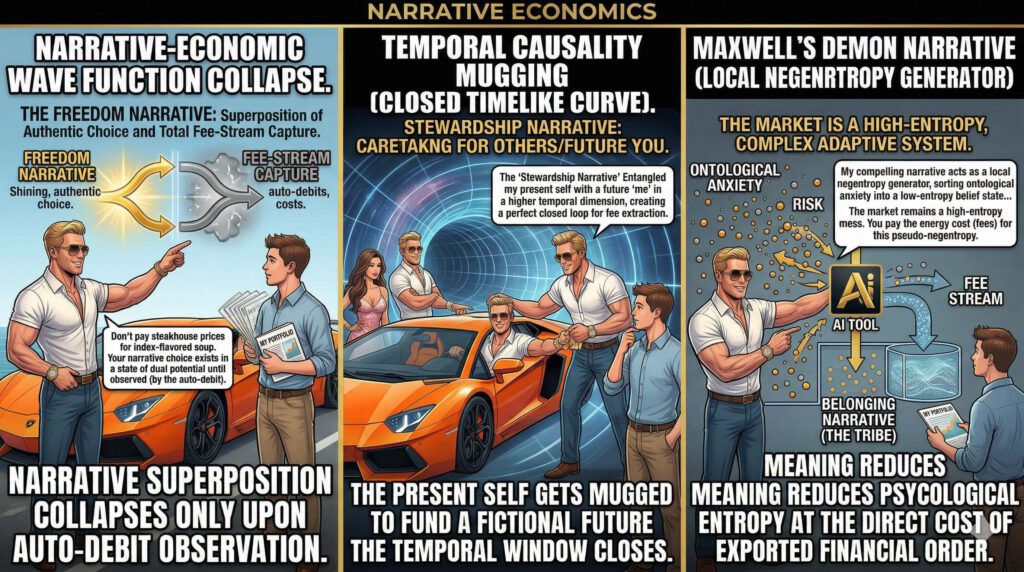

That does not mean all active investing is nonsense. It means fake active investing is nonsense. One of the sharpest ideas in the report is its attack on closet indexing: funds that pretend to be bold while quietly clinging to the benchmark and charging heroic fees for the privilege. If you want alpha, the report argues, you need actual deviation, not expensive imitation. In other words: don’t pay steakhouse prices for index-flavored soup.

From there, the report takes a more philosophical turn and gets much more interesting. Markets are presented not as neat machines, but as complex adaptive systems — nonlinear, feedback-driven, and only partially legible. That matters, because it attacks one of the investor’s favorite fantasies: the idea that enough intelligence, enough data, or enough caffeine can make the future obedient. The report flirts with chaos theory and computational irreducibility to argue that some parts of markets may simply resist compression. You do not solve them once; you live inside them.

This is where the AI discussion avoids both utopian nonsense and anti-tech nostalgia. The report’s stance is refreshingly narrow: AI is probably more useful for research, ranking, filtering, and execution than for grand market prophecy. In plain English, AI may be better at helping you think than at telling you what will happen. That distinction is huge. The report argues that stock picking is easier than market timing, because relative judgments across many securities offer more data and more chances for small edges, while calling the whole market is a one-shot bet against macro chaos. Weather is hard; choosing which roofs leak first is slightly less hard.

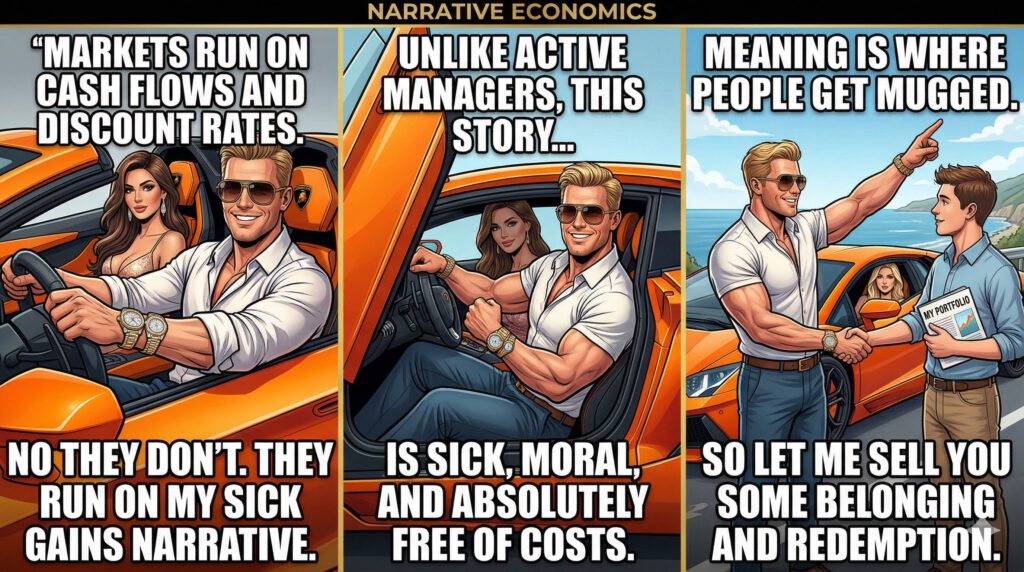

Another very important section is the treatment of narrative economics. This may be the most useful lens in the whole paper. Markets do not run only on cash flows and discount rates; they also run on stories: stories about safety, freedom, progress, expertise, inevitability, belonging, and redemption. Financial products are often sold not as tools, but as identity. The report is excellent on this point: products move money, yes, but they also move meaning. And meaning is where people get mugged. A strong narrative can make a bad product feel profound, urgent, even moral. That is why the philosophical test proposed in the report is so good: would the story still persuade you if it stated the costs plainly?

That skepticism extends beyond asset selection into portfolio construction. The report makes a practical distinction between wealth creation and wealth preservation. Younger or poorer investors may rationally seek more risk because they are trying to build capital; older or wealthier investors often care more about keeping what they already have. This is refreshingly anti-dogmatic. There is no universal “optimal portfolio” floating in the sky above us. There are only portfolios that fit a person’s stage, preferences, and psychological reality. Rationality without human context is often just elegant nonsense.

I also liked that the report sneaks in a broader life philosophy: the point of investing is not to win an abstract status contest. It is to buy independence, then eventually convert wealth into a better life rather than a heavier one. That may be the most underappreciated idea in finance. A portfolio is not a personality. The goal is not to die with the cleanest factor exposure. The goal is to live with enough freedom, enough purpose, and enough emotional slack that markets stop colonizing your inner life.

So what is the practical takeaway from this year’s report?

- First, respect arithmetic. Costs matter more than charisma.

- Second, respect complexity. Markets contain patterns, but not enough to justify permanent certainty.

- Third, respect psychology. Stories sell because people want coherence more than truth.

- Fourth, use AI as a tool, not an oracle.

- Fifth, know whether you are climbing, defending, or simply trying not to do something stupid in public with leverage.

That is why the report is worth reading. Beneath the jokes, memes, and occasional gleeful provocation is a serious claim: good investing is less about brilliance than about avoiding expensive self-deception. Which, admittedly, is a very unsexy slogan. But it may also be the only one with a decent long-term Sharpe ratio.

Download Full Report

Bonus Narratives